The Income-tax Act, 1961 has served as India’s direct taxation framework for over sixty years and , over time, has been amended innumerable times to accommodate the prevailing issues as well as new priorities. However, since the original enactment of the Income-tax Act, India’s economic structure, statute-based structure and technological influence has changed massively. Consequently, Aspects such as globalization, digitalization, new business models and new jurisprudence now require serious consideration and therefore, extensive new measures rather than amendments to the original Act.

BRIEF HISTORICAL CONTEXT: INCOME-TAX ACT OF 1961

The government distributed the Income-Tax Act in 1961 and enacted it on April 1, 1962. Since then, The Income-Tax Act has long formed the basis of India’s direct taxation framework. Since its enactment slightly more than sixty years ago, lawmakers have amended it more than 65 times and introduced approximately 4,000 individual changes. Although they made these amendments to respond to changing economic circumstances, they collectively created a heavy burden, turning the Income-Tax Act into a dense, mysterious, and often contradictory piece of legislation.

This burden of complexity has contributed to extended litigation, interpretational conflicts, and compliance impediments making it increasingly justified to argue for a completely reformed and thereby simplified replacement for the Income-tax Act.

Why the Need for a New Income Tax Bill, 2025

Rapidly, but its tax framework has developed incrementally through modified provisions to the Income Tax Act and through the Finance Act 2022. These provisions established a clear tax framework (30% on profits, 1% TDS on transactions), but there are still a number of holes:

- Lack of regulatory framework – Firstly,Current laws only cover tax, without laws addressing classification, investor protection, or cross-border transactions.

- Treatment of new classes of crypto-assets is unclear – Moreover, NFTs, stablecoins, and DeFi tokens all present unique classes of assets without clear existing definitions.

- Jurisdictional ambiguity for international transactions – In addition, A transaction conducted in cryptocurrency may involve parties from multiple jurisdictions that have different regulatory requirements and tax implications.

- Confusion for retail investors – Consequently, Many retail investors are unaware or uninformed of their compliance requirements resulting in unknowing violations of tax obligations under Indian law.

- Revenue leakage – Finally, The government does not have a sufficient reporting framework to mitigate the loss of tax revenues as transactions may not be reported or reported peer-to-peer.

A new bill could combine taxation and regulation in one seamless law making it a single and clear legal framework that captures innovation, investor protection, and taxation.

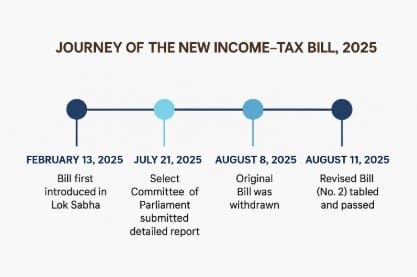

Journey of the New Income-Tax Bill, 2025

Read more about New income tax bill

Read more about differences between old and new law.

Main Issues Addressed in the New Income-Tax Bill, 2025

Taxpayer Confusion & Vague Terminology

The 1961 law included a lot of greyed out areas that generated litigation. With the new Bill, tables have been simplified with defined exemptions and eliminated the redundant language, creating much easier compliance.

High Compliance Costs & Complexity

The old Act included ~819 sections, all over various chapters, making it difficult even for professionals to decipher. The new Bill reduces this to 536 sections and all or most chapters were cut down into 23 sections. The entire legal structure is simpler.

Difficult E – Filings

The reworking of the law includes an e – filing & faceless review for a digital first, upon simply is only using human discretion to increase impartiality, legitimacy, and bracket aside discretion and humanity which affords corruption.

Significant Changes Within The Bill

House Property Defined – The standard deduction held steady, with an addition for claiming “pre-construction” amount for home loan interest on a rented property.

Late filing & there could be a refund claimed – Tax refunds could be done after filing late up to a notice issue to enforce.

Keep the Middle-Class Value – The basic exemption of ₹12 lakh was kept along with slabs reduced to a better position than the salaried group.

Anonymous donations – There are new limits and conditions put on anonymous donations that disconnect charity from individual abuse.

Positives and Potential Drawbacks

| Positives | Concerns |

| Simplified and consolidated law enhances clarity. | Rapid passage without parliamentary debate could affect scrutiny. |

| Easier compliance & fewer disputes via digital systems. | Implementation and tech-readiness may vary across regions/bureaus. |

| Fairer to taxpayers—refundable even post due-date. | Transitional challenges for filers and professionals. |

| Updated norms for pension, house property, refunds. | Some niche groups (e.g., high-income earners) may still feel the pinch. |

Stakeholder Impact Analysis

| Stakeholder | Details |

|---|---|

| Government | -Enhanced legal clarity, enforcement powers -Easier coordination between central and state agencies -Improves India’s compliance with international commitments. |

| Law Enforcement Agencies | -Streamlined investigation procedures. -Access to modern tools and jurisdiction clarity. -Faster prosecution timelines. |

| Judiciary | – Reduced ambiguity in law interpretation. – Potential increase in case load due to broadened definitions. – Needs capacity-building to handle technical complexities. |

| Citizens | – Greater protection of rights and security. – Better grievance redressal mechanisms. – Concerns about potential misuse if safeguards are weak. |

| Private Sector / Businesses | – Clearer compliance requirements and reduced ambiguity. – Possible increase in compliance costs and reporting obligations. |

| International Partners | – Signals India’s proactive stance on global standards. – Facilitates smoother cooperation in cross-border issues. |

| Civil Society & NGOs | – More room to engage in public awareness and advocacy. – May need to push for stronger safeguards against misuse. |

Conclusion: A Modern Tax Code for a Modern India

For India to meet its ambitious economic goals, it requires a taxation system that is efficient, equitable, transparent, and future-ready. A taxation system that is designed for the modern world will allow compliance with the law to be simple, minimize litigation and disputes, and encourage citizens to voluntarily contribute to the state with a high degree of trust.

The system used must also balance raising revenue with promoting economic growth, ensuring that taxes do not impede entrepreneurship, investment, and innovation.

Given the modern economy that is increasingly digital and global, tax laws should use technology to enable administrative efficiencies, enable progressive tax structures that continue to protect the most vulnerable members of society, and adapt to emerging sectors (e.g. e-commerce, gig economies, green industries).

A well-designed tax code can be part of the solution to ensuring inclusive growth in the context of scarce resources; reallocating revenue generated towards critical infrastructure, a greater social safety net, and sustainable development.

If we can keep our processes clear, fair and adaptable – we have a taxation regime that MORES for India’s growth agenda and the social contract between state and citizen. A modern tax code addresses more than just revenue raise – it can get us to a stronger, healthier and more prosperous India.

Do read more blogs about UPSC content at Infotrigg.com

- National Parks for UPSC: List, Latest news and PYQ’s

- Rare Earth Minerals & Critical Minerals – India in the Global Context

- Securities Transaction Tax (STT)– Meaning, Budget Change & Market Impact

- FRBM Act , 2003: Background, Provisions and Significance for UPSC

- Ocean Currents: Causes, Types and Global Distribution for UPSC

I appreciate your research